Open Banking at the Checkout: Why Merchants Are Making the Switch

Ask any merchant where conversion pressure shows up, and they’ll point to the checkout. It’s the moment that decides whether a customer completes the journey or quietly drops away.

Globally, more than 70% of online baskets are abandoned before a payment is made. In the UK alone, that translates into an estimated £38 billion in lost revenue every year. Drop-offs happen for many reasons: failed authorisations, rising card fees, or payment flows that don’t match how customers actually want to pay. On mobile, abandonment rates are even higher, with redirects, delays and hidden costs pushing customers away at the last step.

Checkout failure doesn’t look the same across sectors.

In travel and luxury retail, a failed payment doesn’t just lose the sale; it can undermine the customer’s confidence and derail the transaction entirely. A false decline on a £4,000 watch raises doubts about the merchant’s reliability and potentially causes offence to a valuable customer. A redirect during a holiday booking interrupts the process and often leads to abandonment. These are high-value transactions where customers expect speed, stability and a clear path to completion.

In trading, gaming and gambling, speed drives every transaction. Traders rely on instant deposits to respond to price changes without delay. Gamers expect top-ups to land mid-session so play continues uninterrupted. Bettors want to place a wager and receive winnings within moments. These are high-frequency payment flows where timing shapes behaviour, and where delays can mean the customer doesn’t return.

Beyond the card rails

Many of these drop-offs stem from the way card payments operate - multi-step card flows, 3DS challenges, one-time passcodes and issuer risk checks - add lag and uncertainty, and settlement also takes time to reach the merchant. That’s why merchants in selective sectors are increasingly using Open Banking to improve completion, reduce fraud and speed up settlement.

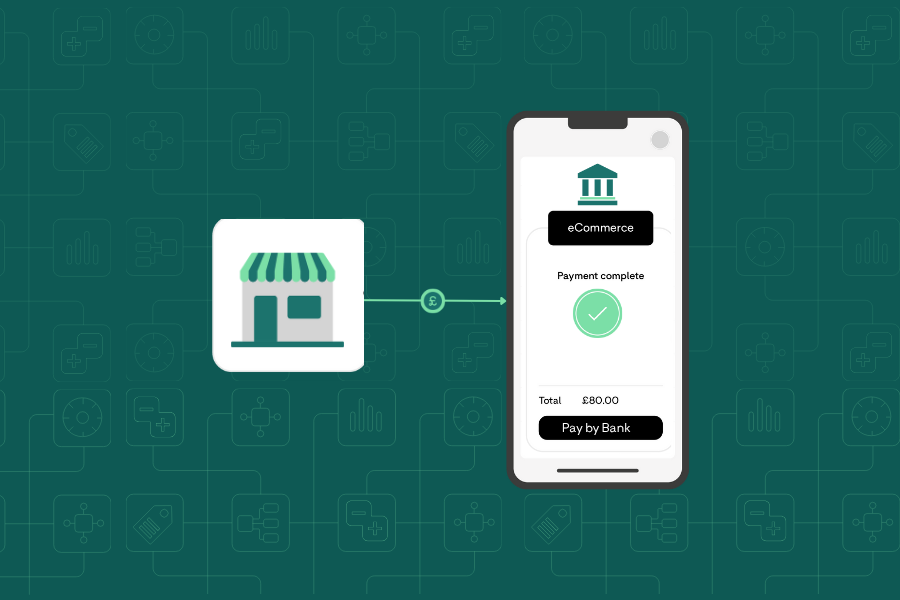

Pay by Bank enables customers to pay directly from their bank account, with authentication handled through their banking interface and settlement completed in real-time. With minimal effort, customers can select the Open Banking payment method, approve in-app and return to the checkout automatically. For merchants, this means fewer intermediaries, faster settlement, and greater control over the payment journey.

Where it’s being used, and why

Open Banking is already live in flows where speed, trust and margin matter most. Travel merchants surface Pay by Bank for high-value bookings to reduce drop-offs and avoid false declines. Trading platforms rely on instant settlement so customers can act on price changes. Gaming and gambling operators use it mid-session to minimise disruption. Instant payouts and withdrawals reinforce trust: high-value shoppers feel protected, and high-frequency users see that funds move both ways without hold-ups.

BR-DGE enables merchants to route to Pay by Bank without rebuilding checkout or switching PSPs. Open Banking providers plug into the orchestration layer, so the method sits alongside cards, wallets and other options. If a bank connection slows or fails, orchestration can route to an alternate provider or fallback method automatically, protecting conversion without manual intervention.

Teams can switch it on for high-value bookings, prioritise it in mobile-first journeys, or offer it selectively in trading/gaming environments where speed drives retention - all without disrupting the existing stack. Coverage spans major UK and European banks in GBP and EUR as standard, with additional markets and currencies added through the same integration as they become available.

Funds settle faster than with cards, improving cashflow and simplifying reconciliation with real-time status updates. Each transaction is bank-authenticated, which eliminates traditional card chargebacks and reduces post-payment disputes. With fewer intermediaries, transaction fees are often lower, especially on high-value purchases. Refunds, including partials, can be initiated via the same connection with status returned in real-time, keeping customers informed.

Adoption is accelerating

In the UK, more than 15 million people and businesses now actively use Open Banking services - close to one in three adults - with 29.9 million payments made in July 2025 alone. Travel merchants are seeing sharp uptake: Trustly reports a 230% year-on-year increase in UK travel spending via Pay by Bank, with European growth led by Germany at 22%.

Across Europe, adoption is rising: market estimates put Europe at around 64 million open banking users in 2024, and the EU’s Instant Payments Regulation - adopted in early 2024 - aims to make euro instant transfers fully available across the EU and EEA, further strengthening the rails that Pay by Bank can ride.

Globally, Open Banking users are expected to surge from 183 million in 2025 to over 645 million by 2029, according to Juniper Research. For merchants, this is a signal that Pay by Bank is becoming a mainstream option across sectors and markets.

TrueLayer, a European Pay by Bank provider, says that 80% of digitally active merchants plan to add the method in the next year.

The merchants moving first aren’t experimenting; they’re editing the checkout to work on their terms. As travel, luxury, trading, gaming and gambling prove out higher conversions, lower fraud and faster settlements, they create a clear pathway for other sectors to follow, with orchestration making it low-risk to switch on, test and scale.

Related content