Payments 101: What is network tokenisation in payments?

Over the past few years, there has been tremendous growth in consumers spending online, but with a positive rise in ecommerce, comes challenges around the sophistication of security measures and fraud.

In a world driven by digital transactions, relying on physical banks with steel walls and complex locks is no longer sufficient to ensure safety from theft. With the increase in online shopping, new vulnerabilities have been introduced that traditional physical security measures cannot adequately address.

Security legislations and technologies have been implemented to protect sensitive information and combat fraudulent activities, with the likes of PSD2, 3DS check, and SCA setting a new benchmark for security of digital transactions.

Whilst existing security measures like legislations and technologies have made significant strides in combating fraud, there is still more that all parties within the transaction can be doing to mitigate fraudulent activity and one of the latest innovations in this field is network tokenisation.

Network tokenisation offers the solution to increasing security, reducing fraud, helping foster trust with customers, and improving the checkout experience.

What is network tokenisation?

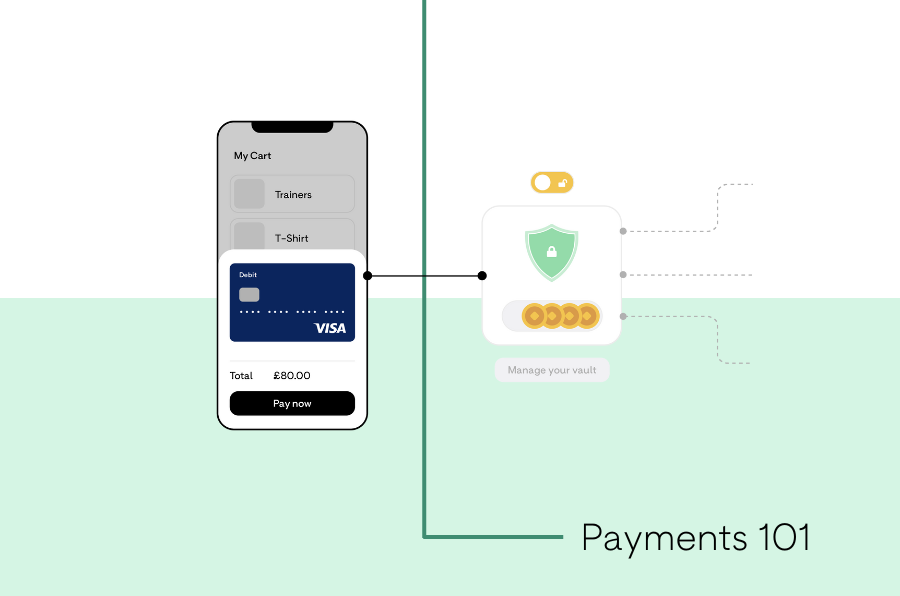

Network tokenisation refers to the replacement of the primary account number by a unique EMV (payment scheme) token, which is restricted to only be used by a certain device, merchant, or transaction type of channel.

By utilising network tokens instead of proprietary (or gateway) tokens, you can ensure card details are protected throughout the entire transaction lifecycle whilst also offering features such as lifecycle management to ensure the card details on file are the most up to date. In addition, network tokenisation opens opportunities for innovative and leading buying experiences across all channels.

What are the benefits?

- Reduce fraud risk in your payment workflow: Security is a vital part of any digital business, and it is especially important when handling personal and financial data. As your eCommerce business grows, so does the risk of fraud. Network tokenisation offers a solution to increase security and reduce fraud by replacing card numbers with a digital token, earlier on in the transaction process. Replacing PANs with tokens reduces the risk from a data compromise event, as without consumer credentials the impact of malware, data breaches and phishing attacks is minimal. Across the payments industry, network tokenisation has been shown to reduce the average fraud rates by around 26% (Visa), without creating any additional friction for consumers.

- Protect consumers from expired PANs: Network tokenisation supports protection from expired PANs, as the token doesn’t expire when the PAN does. This removes frustration from the consumer having to re-enter their card details once their card expires. Network tokenisation allows for lifecycle management; ensuring that lost, stole or expired PANs are updated against a stored token, significantly reducing declines. This supports elevating pass rates by reducing declines for expired card information.

- Gain trust with customers: As digital spending is quite a ‘removed’ experience for customers, feeling secure when increasing online purchasing activity is critical. With 80% of customers abandoning their purchases if they have concerns about security, providing a secure experience is essential, network tokenisation can reduce the uncertainty your customers may feel when purchasing online through your business, therefore increasing trust and loyalty.

- Yield higher authorisation rates. Online payments can fail for a multitude of reasons; entering incorrect details, insufficient funds, expired card details and declined payments. Network tokenisation can reduce the likelihood of a payment failing at your checkout by removing traditional card-on-file barriers and removing irritant layers from expired cards, ultimately elevating higher authorisation rates.

How can network tokenisation with BR-DGE help you design a more flexible payment process?

With network tokenisation anticipated to be a major catalyst in payment innovation, BR-DGE Vault differentiates itself through its Hybrid PAN and Network Token model, a unique token vault proposition that promotes the most relevant token for the payment being made and the processor being used. This helps to ensure Network Tokens are used whenever possible but does not restrict payment optimisation when unavailable.

The BR-DGE payment orchestration platform has an extensive product offering, from network tokenisation services through to intelligent routing, real-time data reporting and access to over 500 connections across the entire payments landscape.

With BR-DGE, we manage all your schemes integrations on your behalf. This not only reduces your transaction costs and resource time but improves the customer’s payment experience.

Accessed via a single API connection, the BR-DGE network tokenisation service ensures the quickest integration to enable you to meet market leading encryption and data security capabilities. With our modular solution, our network tokenisation services can be consumed alone or alongside our orchestration suite, allowing you to scale a payment solution that suits your payment needs.

To find out more about network tokenisation and how BR-DGE could support you in reducing data breach risk and foster trust with customers, get in touch with the team

Related content