When cards fail: How Open Banking can rescue lost revenue

Card payments remain the primary way customers pay online, yet they’re also where many sales fall over. An issuer decline, input error or a failed authentication step can kill the payment, even when the customer is ready to complete it. These failures lose sales that merchants can rarely recover.

For merchants, this is a routine problem. Card failures chip away at revenue every day, and most checkouts give customers no simple way to complete the payment once the card attempt fails.

Why declined payments are hard to recover

Most checkouts follow one fixed route. The customer picks their card, the attempt runs, and if it fails, the checkout simply stops. The customer sees an error and ends up back at square one. On mobile, that often means re‑entering details or repeating authentication, and many people simply drop out instead.

It mostly comes down to how payment stacks are structured. The card route is locked in early, and the checkout can’t easily switch to anything else once the attempt runs. Payment Service Provider integrations limit flexibility, and most checkouts are still built on fixed logic.

So, when the card fails, the checkout has nowhere else to go. The customer leaves, and the sale disappears with them.

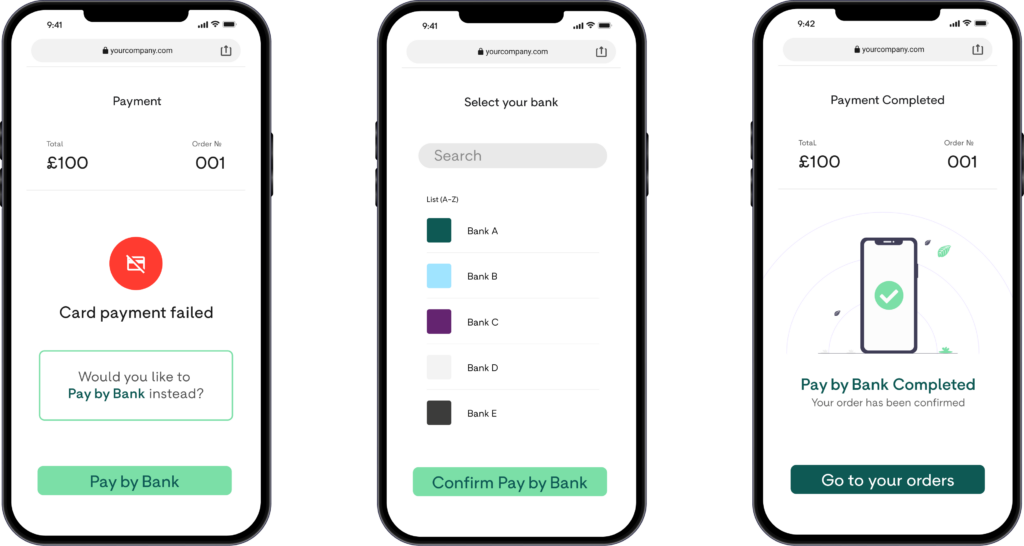

Open Banking as a recovery rail

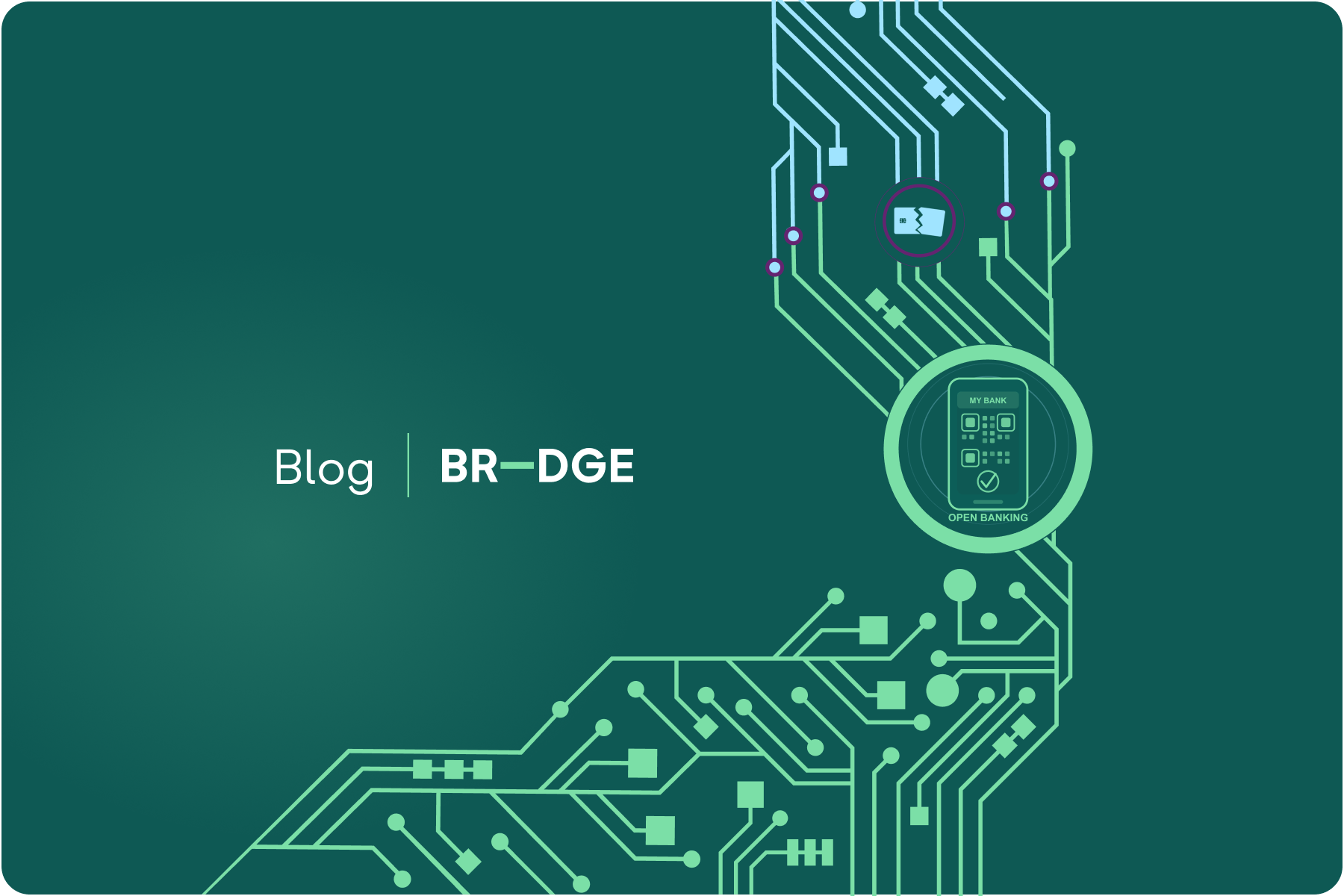

Open Banking can potentially give merchants a way to keep the sale alive when a card drops out. Instead of sending the customer back to the start, the checkout can surface a direct bank payment that’s authorised through the customer’s banking app. It’s a real-time account-to-account transfer, so the payment runs straight from their bank with strong customer authentication built in. Provided the customer has the method set up, there’s no additional approval steps and no card network dependency, or lengthy chain of providers involved.

For the customer, the payment journey can continue even when the card route has failed. The intent to buy is still there, and the checkout can offer a clear way to complete the purchase without starting again. What might have become abandonment can still turn into revenue, with a bank payment sitting alongside cards as a practical fallback.

Because the payment avoids the points where card transactions typically fail, it acts as a resilience layer as well as a recovery rail. It keeps high-intent customers in play, reduces abandonment, and gives merchants a practical way to protect conversion. It looks something like this:

Where this approach works best

Open Banking works best in moments where the customer already intends to complete the payment and has sufficient funds available. High-intent transactions are a strong fit because the customer has already committed to the purchase and simply needs a reliable way to finish it.

For instance, a customer reaches the final step of a £180 trainer purchase. The size is in stock, the delivery window works, and they’ve already committed to the order. The card attempt drops out during authentication and the checkout returns an error. With no alternative route, the customer abandons the purchase and the stock sits in the basket until it times out..

With a bank payment sitting alongside cards, the checkout can surface a direct bank route the moment the card attempt fails. The customer approves the payment in their banking app and completes the order without restarting anything.

Repeat customers also benefit. They already trust the brand and want a quick way to complete the purchase. A direct bank payment gives them a fast route to finish the order when a card attempt fails.

Merchants can also win from this approach on a different level. Once a customer has opted for Pay by Bank once, they are more likely to do so again, which supports adoption. This is an advantage for merchants - the fee structures, settlement certainty and lower fraud rates can make bank payments a very cost-effective method.

Why infrastructure matters

Decline recovery only works when the checkout can move to another payment instrument instantly. That depends on the infrastructure underneath. A flexible setup can introduce a bank payment the moment the card route falls over, keep the customer in the flow, and complete the order without reworking the underlying payment flow.

Orchestration plays a central role here. It gives merchants control over how payment attempts are handled and creates room for the checkout to adapt. When the system can route the payment to another rail instantly, a failed card attempt becomes a recoverable moment rather than a lost sale.

This approach also strengthens resilience. A multi‑rail setup gives merchants more ways to keep payments moving. It creates room for the checkout to shift routes instantly and maintain steady conversion across different markets and customer groups.

The shift to payments becoming multi‑rail

More merchants are building payment setups that can draw on more than one route to complete an order. A multi‑rail approach gives the checkout room to adapt in real time and keep the payment moving even when the first attempt drops out. It creates a steadier path to conversion, works more reliably across markets, and gives customers a smoother way to finish the purchase.

Open Banking brings a direct bank route into the mix and gives merchants another way to complete the payment when the first attempt fails. As more payment flows become dynamic and orchestration takes a larger role, the ability to move between rails becomes a commercial advantage rather than a technical detail.

The result is a payment system that protects revenue, supports growth, and gives customers a clearer path to complete the order. Multirail is becoming the standard for merchants who want a checkout that adapts, performs, and keeps high-intent sales in play.

Related content